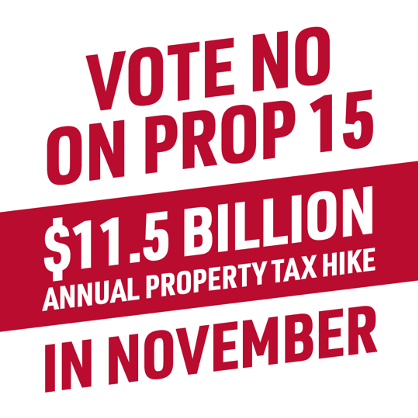

California is in the midst of an unprecedented economic crisis, and yet another threat is on the horizon. The 2020 California Proposition 15 would change the way commercial property is taxed and have a devastating effect on small- and medium-sized business that make up half of California office tenants.

Proposition 13 was approved by 65% of California voters in 1978 and currently limits property tax reassessments (increases) to 2% annually but allows for full tax reassessments if the building is sold, more than 50% is transferred, or substantial new construction is completed. Significantly, 2020 California Proposition 15 (aka “split roll”) would remove the 2% reassessment limit and require commercial and industrial properties to be taxed based on their market value beginning in fiscal year 2022-2023. In California, commercial landlords in multi-tenant buildings typically pass on a pro-rata share of building operating expense (OPEX) including property taxes, to their office tenants. In the most common office lease, tenants are only responsible for OPEX increases over the “base year” amount which is most often the year of the commencement date or the year following the commencement date. Property Tax Liability As tenant representatives, we advise our clients that ownership matters. The differentiator between two similar buildings and spaces with like amenities and rent can often come down to the quality of ownership. Buildings that have been owned and managed by the same entities for a long period of time tend to be better managed. Under Proposition 13, buildings like these may not have been reassessed at market value for years and in some cases decades. As a result, their tenants carry a large tax liability if the property is sold or transferred during the term of their lease. Or, if Proposition 15 passes. How much will tenants absorb when Proposition 15 tax increase is passed through to them? Let’s keep the math simple for this hypothetical example and use a 1.15% property tax rate and assume that you entered into a 7-year lease for 10,000 rentable square feet (RSF) in a San Francisco building with ~500,000 RSF. You would have a 2% pro-rata share with a 2019 commencement date and base year. In this example, the building hasn’t been sold since 1998 and has a Proposition 13 assessment value of $75,000,000 in your 2019 base year with property taxes of $862,500. When the assessment value of the property is increased by the Proposition 13 maximum of 2.0% in 2020, the subsequent year’s taxes will be $879,750. You will have to pay your 2% share of the $17,250 increase over base year, or $345. In 2021, taxes will be $897,345 and your 2% share of the $34,850 increase would be $697. All very manageable. However, in 2022 under Proposition 15 the 2% limit on property tax reassessments is removed and property will be reassessed and taxed on the market value of $400,000,000 (estimated $850/SF sale price) with property taxes increasing to $4,600,000. The increase in property taxes from your base year 2019 to 2022 would be $3,737,500 and since your company occupies 2% of the building, you’ll get handed a bill for $74,750. And, on top of your base rent you’ll pay that bill and more every year until your term runs out. How many CEOs would knowingly take on a contractual obligation without the ability to control, or plan for cost increases? Whether Proposition 15 passes or not, California office tenants still carry a large tax liability if the property is sold or transferred during the term of their lease. Just as we advise our clients that ownership matters, so too does a building’s property tax liability. In addition to ownership, the differentiator between two similar buildings and spaces with like amenities and rent may come down to size of a tenant’s property tax liability. For this reason, we pursue some level of protection for our office tenants by seeking a limit on Operating Expense increases throughout the term of the lease. For the last decade only the largest tenants in softer markets have been able to negotiate caps on OPEX increases. But a black swan event like the coronavirus pandemic shifted leverage in markets that once favored landlords to favoring tenants overnight. Seeking and obtaining OPEX protection is easier said than done but it should always be subject of negotiation. At a minimum, it’s important to do the math on your reassessment liability before entering a lease in any building in California. Tenants need to know when the property was last reassessed for Proposition 13 purposes, what its assessed value was, and what its assessed value is today in order to forecast the potential liability due to a transfer of ownership or passage of Proposition 15. The longer it’s been since the last reassessment, the greater your exposure to property tax increases. Comments are closed.

|

Archives

June 2024

Categories

All

|

RSS Feed

RSS Feed